As a community organization, educating society on various aspects of civic life in the United States of America is part of Bay Malayali’s social commitment. To this, we make short films, seminars and much more… The points we expected to cover are :

| Financial Planning | based on the rules and regulations of the United States of America is often overlooked by most migrants due to various reasons. Also, the rules of inheritance vary from state to state and the impact of being in a community state vs independent state also varies. These laws are far different from that of India. The impacts of inaction are not well understood by most and often not discussed in our community. The targeted audience of this page is recent migrants who have not gone through the proper financial protocol. |

| Intestate |

If you die without a Will, it means you have died “intestate.” When this happens, the intestacy laws of the state where you reside will determine how your property is distributed upon your death. This includes any bank accounts, securities, real estate, and other assets you own at the time of death. Real estate owned in a different state than where you resided will be handled under the intestacy laws of the state where the property is located. The laws of intestate succession vary greatly depending on whether you were single or married, or had children. In most cases, your property is distributed in split shares to your “heirs,” which could include your surviving spouse, parents, siblings, aunts and uncles, nieces, nephews, and distant relatives. Generally, when no relatives can be found, the entire estate goes to the state (This often happens when H1 folks have no heirs in the country to navigate through the probate process as H4 spouse has to leave the country quickly and often no way to comeback). |

| Joint Accounts | Bank Accounts and other assets have ownership and title established under two or more names to ensure easy succession. Details below. |

| Will | coming soon |

| Living Trust | coming soon |

| Life Insurance | coming soon |

| Organ Donation | coming soon |

| Advance Directives | coming soon |

| Probate Process | The standard process by which a court determines the assets and liabilities of an individual, and distributing the remaining estate by a court-appointed executor.

Details -coming soon |

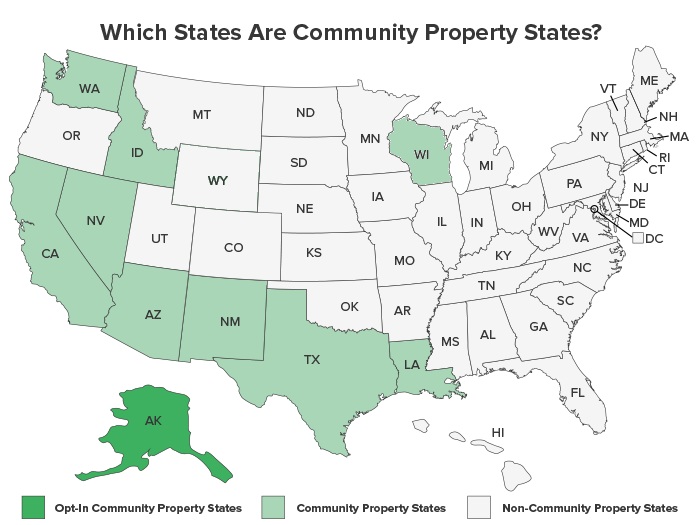

| Community States | The states having community property are Louisiana, Arizona, California, Texas, Washington, Idaho, Nevada, New Mexico, and Wisconsin. Community property states follow the rule that all assets acquired during the marriage are considered “community property.” |

| Prenuptial Agreement | coming soon |

Joint Bank Accounts

A joint account is a type of bank account that allows more than one person to own and manage it. There is no restriction regarding who can be an owner. Everyone named on the account has equal access to funds, regardless of who deposited the money.

Joint bank accounts aren’t for everyone, and the rules for how your money is handled in the event of death or divorce vary depending on the type of joint account you open and your state’s laws. Below, we discuss the various factors to consider when opening a joint account, along with a comparison of its different forms, instructions for opening an account, and advice on how to manage it well.

| Pros | Cons |

|---|---|

| Probate Process can be bypassed If your joint bank account carries a right of survivorship in the event of an owner’s death. Probate can be a costly and time-consuming procedure, a joint bank account with a right of survivorship can help make sure funds are available to pay bills without delay after one party’s death.

Equal Ownership: Any owner can draw or deposit funds without the involvement or consent of the other owners. |

If your account carries a right of survivorship and you die, your account will not be included in your estate and therefore will not honor any instructions in your will, if you have one. This can be an unintended consequence if you meant to leave your money to your heirs (eg: Parents, Siblings, children), not to your co-owner (Spouse).

Joint Liability: Everyone is liable if one owner mismanages the account (e.g., overdrafts), and everyone may be reported to ChexSystems |

| Additional Deposit Insurance: Joint account with two owners enjoy up to $500,000 of FDIC deposit insurance, guarantee compared to $250,000 for an individual account. | No Individual Protection: Legal action may be necessary to recover funds if one owner depletes the entire balance and closes the account. |

| Simplified Finances: Paying shared expenses out of one account can make budgeting and paying household bills easier. | Limited Asset Protection: Depending on your account terms, a creditor can collect against the joint account to satisfy the debt of one owner, regardless of who deposited the money |

| Strict Account Closure Rules: Any owner can close the account but cannot remove another owner without that person’s permission. | Gift Tax Issues: Any amount exceeding $14,000/year that is withdrawn by an added co-owner (other than your spouse) may be treated as a gift by the IRS (also applies if you add a co-owner before death, which may subject you to estate tax). |

| — | Divorce Issues: If you split up with your spouse, you’ll continue to share the account until it’s closed. The spouse of your co-owner going through a divorce may also be entitled to funds in the account, regardless of who deposited the money. |

Right Of Survivorship

One distinct feature of a joint bank account that is not common among other account types is a “right of survivorship,” which is an option on all standard joint bank account forms. A right of survivorship stipulates that if one owner dies, 100% of the remaining balance passes to the surviving owner. This can be both a blessing and a curse, and here’s why:

Benefit: If your joint bank account carries a right of survivorship, the account bypasses probate in the event of an owner’s death. Because probate can be a costly and time-consuming procedure, a joint bank account with a right of survivorship can help make sure funds are available to pay bills without delay after one party’s death.

Open The Right Type Of Account: If you intend to leave your money to someone other than your co-owner upon your death, name that person as a beneficiary on a payable-on-death (POD) account. Keep in mind that there are other options besides joint accounts that may suit your needs better. If you need help with banking activities, for example, you can get a “durable power of attorney” that maintains your ownership of the funds and limits your “agent’s” access to your account to certain circumstances (e.g., incapacitation). Special accounts called Uniform Gifts to Minors Act (UGMA) and Uniform Transfers to Minors Act (UTMA) accounts are designed specifically for minor children. With these accounts, you can save money on behalf of your child as a custodian until he or she reaches age 18.

Risk: If your account carries a right of survivorship and you die, your account will not be included in your estate and therefore will not honor any instructions in your will, if you have one. This can be an unintended consequence if you meant to leave your money to your heirs, not to your co-owner.

However, there are several types of joint bank accounts (see next section) that do not have a right of survivorship or for which you can opt-out of this option. Some circumstances can also dissolve a joint account’s survivorship status and the assets become subject to a will, depending on your state’s statute. We recommend consulting an experienced estate planning attorney if you want to learn more about these special cases.

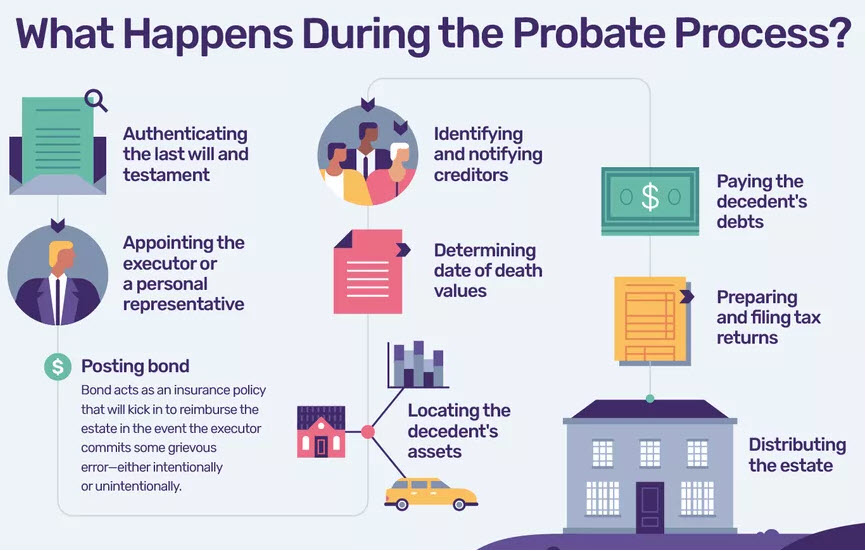

Probate Process

Probate is the court-supervised process of authenticating a last will and testament if the deceased made one. It includes locating and determining the value of the person’s assets, paying their final bills and taxes, and distributing the remainder of the estate to their rightful beneficiaries.

If you need more help or guidance, please email BayMalayali@Gmail.com

BayMalayali is not a certified financial advisor or planner and any information provided here is based on the public information available online. Bay Malayali or its board of directors or office bearers are not be held responsible . Reference credits to: https://estate.findlaw.com/ , www.thebalance.com, & https://wallethub.com/